Assad’s Fall and the Qatari Gas Pipeline: A Risky Bet or Potential Source of Relief?

Assad’s Fall and the Qatari Gas Pipeline: A Risky Bet or Potential Source of Relief?

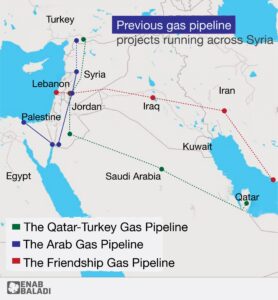

Two days after the overthrow of Syrian President Bashar al-Assad, Turkish Energy Minister Alpraslan Bayraktar announced that Ankara was considering resuming construction of a pipeline that linked Qatar’s North Field gas reserves to Turkey’s Trans Anatolian Pipeline (TANAP) network via Saudi Arabia, Jordan and Syria. The announcement was largely drowned out over the next several weeks by the flurry of diplomatic delegations that visited Syria and pledges by foreign governments to provide aid and renewed investments to revive the country’s ailing economy.

If built, the pipeline would be the most consequential development to occur as a result of Assad’s ouster, bringing significant potential benefit to the EU. Today, the EU imports nearly 15% of its natural gas from Qatar and is also the primary market for gas delivered via TANAP, mostly from Azerbaijan. Rerouting Qatari gas via TANAP would make EU imports cheaper and more reliable as it accelerates the bloc’s transition to net zero by preventing supply shortages that could hinder the buildout of renewable infrastructure and electrification of the continent’s energy grid. It would also reduce China’s growing dominance within the global LNG market by potentially crowding out Chinese LNG resold in Europe.

Following Russia’s 2022 invasion of Ukraine, Europe managed, in part, to avoid energy shortages by increasing imports of LNG purchased and resold on international spot markets by Chinese middlemen. That year, China became the world’s second largest LNG reseller after Spain, exporting 1.7m tons of mostly US and Russian LNG to European and Asian buyers. China’s resale of LNG is possible because of the significant discounts it receives on U.S. and Russian imports relative to other buyers.

Starting in 2021, China signed numerous long-term purchase agreements with American suppliers indexed to the U.S. Henry Hub, which offers lower rates than European and Asian markets. These agreements did not include final-destination mandates—a practice introduced by the United States in 2015—enabling Chinese state-owned firms to take advantage of the price premium to reap hundreds of millions in profits through resale.

Starting in 2022, Moscow granted Chinese buyers 30 to 50% discounts on LNG, prompting the latter to expand its Russian imports by 28.7%. Despite sluggish growth, China continues to seek new long-term fixed rate contracts to satisfy growing demand that is expected to increase another 50% by 2040, locking China in as the actor with the most influence over world LNG supply for the foreseeable future.

Some of these purchases appear to be aimed at converting China into an international storage and delivery hub for LNG. The growth of such a market could enable China to settle contracts in RMB, contesting the petrodollar’s dominance in the energy sector, and helping to insulate Beijing from U.S. sanctions in the event of military escalation in the Taiwan Straits or South China Sea.

Construction of a Qatari-Turkish pipeline through Syria could help stall or avert such a scenario, and potentially reduce Beijing’s geopolitical leverage over a critical energy sector. However, running a new pipeline through Syria carries its own risk, particularly as the country’s new government begins to take shape.

Syria’s Gas Gambit

First proposed in 2005, former Syrian President Bashar al-Assad vetoed construction of the Qatari-Turkish pipeline on Syrian territory in 2009, due to Russian pressure. Supported at the time by ExxonMobil and Total, the pipeline was one of three proposed in the early 2000s that aimed to connect Middle East gas reserves to Europe via Syria as alternatives to Russian gas, alongside Egypt’s Arab Gas Pipeline and Iran’s Islamic Gas Pipeline projects.

The outbreak of the country’s civil war in 2011 indefinitely ended all prospects that new energy infrastructure would be built in Syria. However, with Assad gone, Qatar and Turkey may be able to pursue construction of the pipeline unobstructed for the first time in 20 years, as both countries have long standing ties to Ha’it Tahrir al-Sham (HTS) —the country’s de-facto governing authority— and other Syrian rebel factions.

The euphoria brought about by Assad’s removal and the end to Syria’s 13-year civil war has furthermore generated significant enthusiasm in the region and in the West for the lifting of sanctions, both on humanitarian grounds and for the economic benefits that would accrue to companies that take part in the country’s reconstruction.

On December 16, 2024, Chairman of the Senate Foreign Relations Subcommittee on Near East, South Asia, Central Asia and Counterterrorism Chris Murphy called on the United States to consider lifting sanctions on Syria entirely on the grounds that the government they were meant to pressure is no longer in place.

On January 06 2025, the U.S. Treasury issued a 6-month license lifting restrictions on remittances and energy sales to Syria, an exemption to sanctions included as part of the Caesar Syria Civilian Protection Act, which Congress extended to 2029 on December 12, 2024 as part of the National Defense Authorization Act.

In June 2025, the Trump administration will be left with the decision on whether to extend, expand, or end Syrian sanctions relief. This is a decision that will likely depend to some degree on the extent to which HTS adapts to international norms and abandons its roots as a Salafi-Jihadist organization. The administration should be cleareyed about balancing the benefits against the potential downsides of lifting sanctions and enabling Syria’s rise as a regional energy hub. There are many concerns.

Turning Syria into a regional energy hub, with power over an ever-growing share of Middle East supply, would further increase the group’s (HTS) leverage throughout the region.

For starters, construction of a pipeline through Syria would carry obvious national security concerns, as HTS and other Salafi-Jihadist groups integrated into Syria’s new government could earn significant revenue in transit fees that could be used to finance jihadist networks. By hosting such a pipeline, HTS could also acquire the ability to regulate and potentially embargo a portion of Europe’s energy supply. This situation might create a massive source of geopolitical leverage never before wielded by a Salafi-Jihadist group.

Furthermore, should regional states continue their process of normalization with Syria’s new government, the construction of a Qatari-Turkish pipeline would likely set a precedent that might encourage Egypt, Iran, and other states to consider relaunching the projects they put on hold after 2011.

Despite both being adversaries of Syria’s new administration, Egypt in particular may be able to use the prospect of a lucrative and mutually beneficial energy project as a way to repair relations with HTS following years of providing support to the Assad regime. In such a scenario, turning Syria into a regional energy hub, with power over an ever-growing share of Middle East supply, would further increase the group’s leverage throughout the region.

Practical challenges must also be considered when assessing whether to support the construction of a new pipeline. Unlike spot markets, it is standard for importers of pipeline gas to commit to sign onto years or decades long purchase agreements with suppliers. This requirement would likely undermine the EU’s net-zero commitments and contradict the bloc’s goal of phasing out rather than expanding reliance on fossil fuels.

This desire to avoid long-term purchase agreements is in part what has driven the EU to rely so heavily on LNG spot markets as alternatives to Russian gas. However, rather than avoid Moscow altogether, reliance on LNG has created the space required for China and other non-producing nations to emerge as important middlemen in the global energy market.

Liquid Renminbi, Liquid Gold

The reach of the U.S. sanctions regime along with dominance of the petrodollar is largely possible because of the market for oil futures and derivatives, which dwarves the trade in international physical oil cargo by a factor of nearly thirty. Following the imposition of U.S. sanctions on Russia’s shadow fleet and the associated value chain in 2022, global traders lined up behind Washington for fear of risking their dollar-based futures contracts, leaving Moscow with few options to offload its exports.

Beijing understands the risk posed to its own energy sector by the petrodollar’s dominance, particularly should western countries impose sanctions on China in response to the latter’s military aggression in the Taiwan Straits or South China Sea. China attempts to insulate itself against this risk by diversifying the type, trade partners, and delivery methods of its energy imports, as well as encouraging the use of RMB in settling contracts.

China’s growing role as an LNG re-exporter suggests Beijing may also seek to transform itself into an international liquid delivery and storage hub which can facilitate the development of futures contracts tied to physical cargo that can serve as an alternative to the US Henry Hub index.

In so doing, China would be replicating the trajectory of Brent Crude, which emerged in the 1980s as the marker for crude oil not because of production points, but because of the emergence of a large liquid delivery point. China’s recent activities suggest this may be part of its strategy: even as its imports of LNG continue to increase, local utilization rates remain low.

Rather than avoid Moscow altogether, reliance on LNG has created the space required for China and other non-producing nations to emerge as important middlemen in the global energy market.

China is currently ramping up construction of storage facilities, introducing the world’s largest onshore LNG storage tanks in 2024 as part of the CCP’s Five-year Plan to double LNG storage capacity by 2025. China is also increasing production of LNG tankers, giving its trading companies greater control of growing trade portfolios, and positioning China as the arbiter of LNG in the still-developing global market.

As the trading arms of Chinese state-owned energy giants buy up long-term U.S. LNG contracts at low prices and re-sell it on the spot market to buyers in Europe and the developing world, it does more than pocket tremendous profits off the arbitrage. It positions China to become a hub for both a physical and paper trade, potentially creating an opportunity to price and settle contracts in its own currency.

This would help China meet its dual goals of insulating itself against exposure to the risk of U.S.-led energy embargoes while undermining the petrodollar’s dominance that affords Washington geopolitical leverage in energy markets. Shielded from such leverage, a more emboldened and assertive China may find itself more willing to risk a military conflagration in the region, either in Taiwan or elsewhere in the near Pacific.

Short and Long-Term Prospects

Either way, the U.S. and the EU are both stuck weighing the least costly of the available options. If the pipeline is not built, it will be business as usual: Europe’s rising demand for Chinese-brokered LNG combined with Chinese dominance in clean energy technologies is gradually replacing energy dependence on Russia with energy dependence on China.

If the pipeline through Syria does move forward, it helps Europe mitigate both problems, but the geopolitical power that accrues to the Syrian regime may be beyond the level of acceptable risk. This scenario is also likely to free up more LNG to meet rising demand in the Global South, but this is still likely to go through China unless the U.S. gets serious about long-term partnerships and overseas investment in energy infrastructure.

Purchasing long-term contracts directly from U.S. brokers would solve the bloc’s geopolitical woes, but not without adjusting the EU’s net-zero climate agenda which requires European states convert 45% of its energy supply to renewables by 2030 and phase out fossil fuels entirely by 2050. Inherent in this requirement is a paradox, as building out an electrified grid and renewable infrastructure is itself an extremely energy intensive process that for now can only be achieved primarily by relying on fossil fuels.

Perhaps for this reason, despite the fallout from Ukraine, between 2023 and 2024, Germany quietly increased by 600% its purchase of Russian LNG, which is not subject to the same sanctions as Russian pipeline gas. In the long term, it may make more sense for the EU to adjust its net-zero commitments and opt for a more reliable long-term partnership with the United States. Failure to do so appears inevitably doomed to benefit America’s top adversaries and foes.